Bonds Don’t Like the Inflation Backdrop

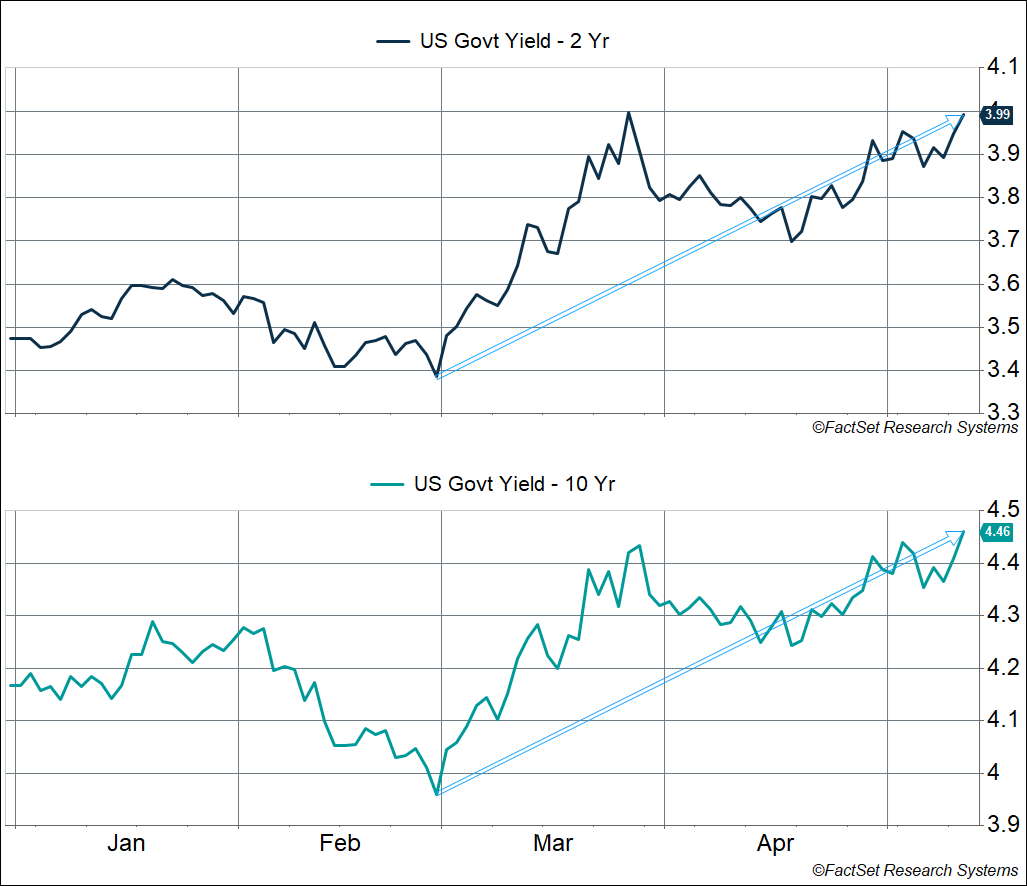

The most direct impact of the inflation backdrop is on the bond market. Short and long-term yields are at the highest levels we’ve seen this year and reflect the real cost of the Middle East crisis and underlying inflationary heat. US Treasury 2-year and 10-year yields have risen to their highest levels this year, even with the equity market reaching all-time highs:

- The 2-year Treasury yield has risen from 3.37% on the eve of the war to 3.99%.

- The 10-year Treasury yield has risen from 3.94% to 4.46%.

Keep in mind that bond prices fall when yields rise.

Seeing the 2026 trend, we are in an inflationary growth environment. It’s not great for bond yields and general borrowing costs. The labor market is also holding up, and normally, we would be talking about rate hikes. However, the Federal Reserve under new Chair Kevin Warsh is expected to hold rates steady for the rest of the year, rather than raise them. That’s a potential tailwind for stocks, on top of the fact that a lot of the profit growth you’re seeing is the other side of the inflation coin. After all, one company’s margin expansion (and profit growth) is another person’s inflation.