AAK is a manufacturer and specialist in vegetable oils and fats. It is what is called a refiner .

The company was founded in 2005 and today has about 4,100 employees and 20 production facilities in many different countries. One of the characteristics of the companies is that they have been skilled at expanding globally over time. We have seen many other companies fail there. In short, you can say that AAK is in the middle of the chain, right between the farmers and the actual producers of daily goods that are then used by the consumer.

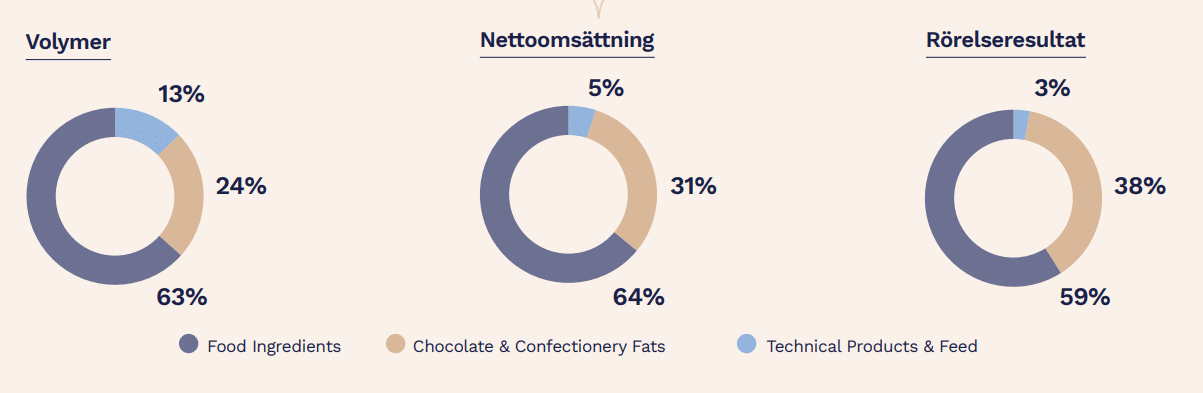

The business is divided into three different departments

- Food Ingredients . The majority of which is aimed at bakery, dairy and a lot of other things.

- Choclate & Confectionery Fat. Accounts for 31% of sales and offers mainly products for cocoa butter and specialty fats for confectionery. It also targets personal hygiene

- Technical Products & feed. Is the smallest part (5% of sales). Here we find, among other things, plant-based candle wax and animal feed.

The most common raw material that AAK purchases is palm oil. As we are a refiner ourselves who pass on the prices to our own customers, we are not directly dependent on raw material prices, even though it indirectly affects the company.

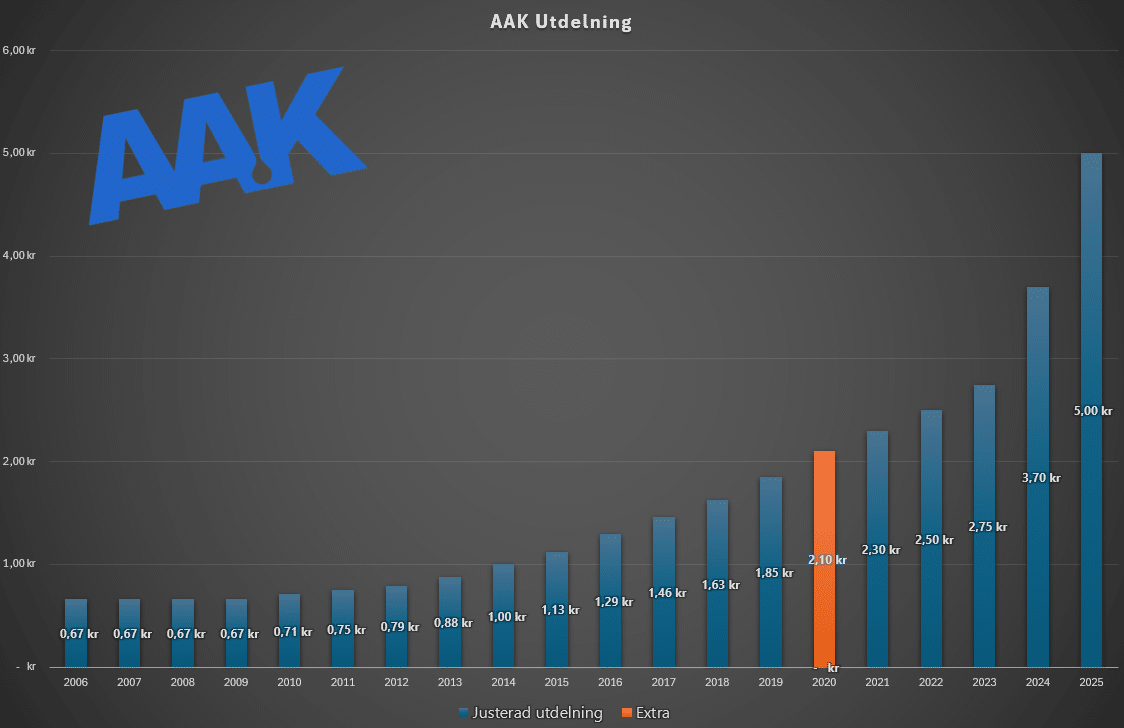

The dividend yield is 1.86% . Sure, that’s not a big number, but given the company’s growth story, we can hardly expect higher numbers.

The forecast is that AAK will distribute SEK 5.5 in 2026 and then SEK 6.0 in 2027. It is just a forecast and AAK could just as easily sweep in higher figures. The good thing is that profit/share in 2024 was SEK 13.62. Of this, only SEK 5 is distributed. In other words, you have a lot of dough to invest in your own business. This is needed when you are constantly on your toes to grow more.

A stock worth buying now?

Here is a summary of the most important points raised in the analysis:

- The company is in a kind of megatrend where plant-based oils and fats are taking over from animal fats as customers want to focus on sustainability. A bit like plastic is now gradually being replaced by paper products.

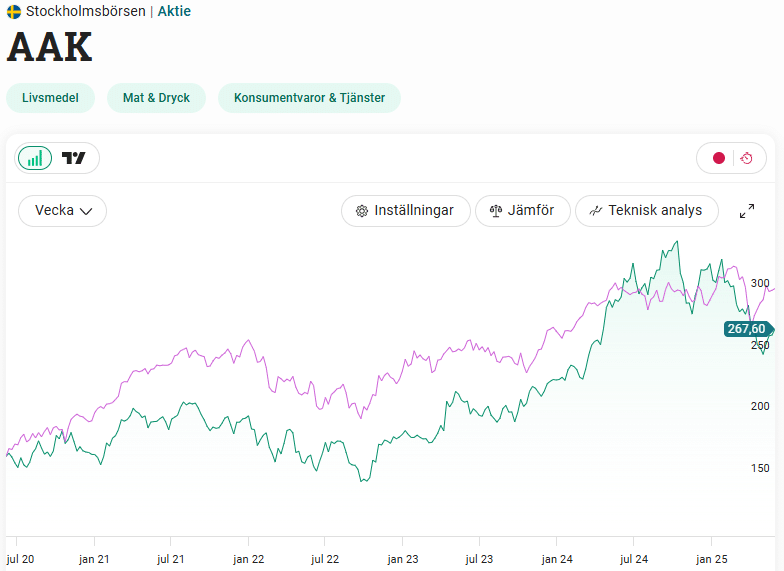

- The stock has fallen a lot, but the business is doing very well. This has caused the P/E (current year) to drop from about 30 to 18. In other words, a halving.

- The reason the stock has been weak is partly Trump’s statements but also the Q1 report which contained some weaknesses but absolutely no long-term concerns. Among other things, volumes decreased organically (excluding acquisitions) by 5%. Despite this, profit per kilo increased by 11%.

- AAK has given 11.3% in total return annually over the last five years. But considering how the profit has increased, it seems low. And yes, if you look at how the operating profit per kilo has increased over the last 5 years, the market may have been a little too restrictive in raising the share price.

- The company has very low debt. The goal is for the debt ratio (debt divided by EBITDA) to be below 3.0, but today it is 0.43. This gives a lot of room for acquisitions and expansion.

- In recent years, AAK has improved its operating margin from 6-7% to almost 11%. A major reason is that it has become better at special products where the margins are simply better than the more classic ones.

AAK is clearly a stock that should fit well into a portfolio where the investor is looking for growth. The company can most likely continue its success story for many years to come and the stock should sooner or later follow along on the journey.

I certainly considering to start investing in AAK looking at today’s P/E.