*US focused article (might be valid for other markets too)

Over the last 5 years (2021-2025), the Consumer Price Index (CPI) has averaged a 4.5% annual inflation rate. The Federal Reserve’s (Fed) preferred inflation metric, the Personal Consumption Expenditures Price Index (PCE), has averaged 4.0%.

The Fed’s official target is 2%. They haven’t gotten close to that in five years, and it doesn’t look like they’re going to any time soon.

We’re still getting inflation data from a couple of months ago (January). But it’s useful to gauge where things were prior to the current crisis, and inflation was already moving the wrong way.

Headline and even core numbers can hide what’s happening under the hood. Core inflation has certainly been pulled higher by tariff-impacted goods and even higher stock prices.

Long story short, the inflation picture was not pretty prior to the Middle East crisis. And it’s going to get a lot worse.

Only Energy Shock?

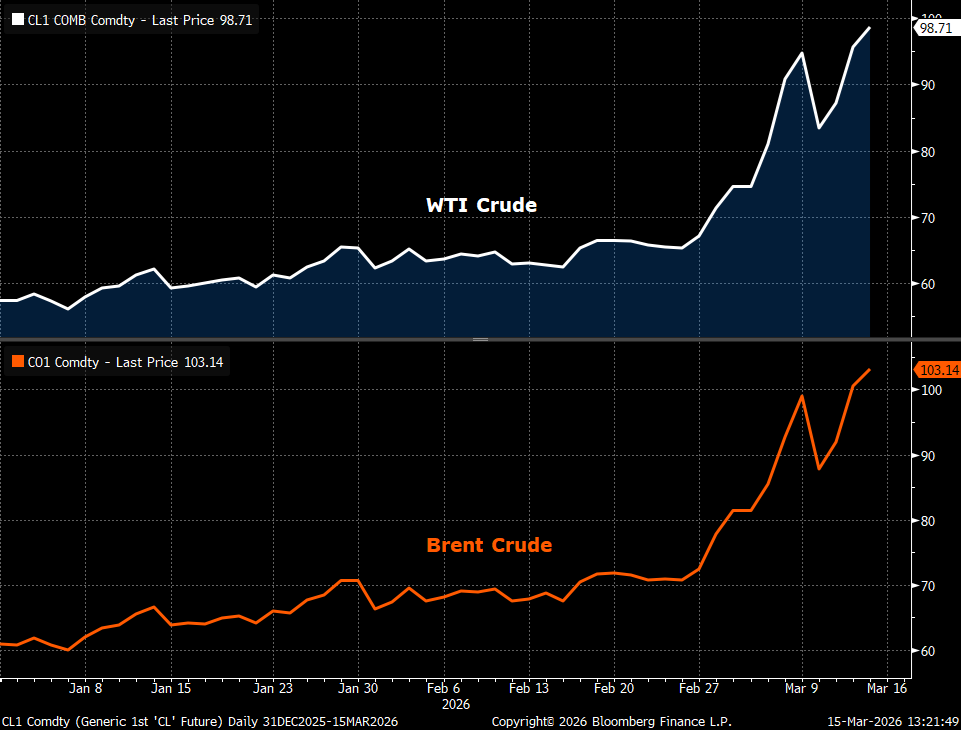

It won’t be a surprise to see all the inflation readings jump next month on the back of oil prices. Oil prices were already rising in January and February, and have surged even more over the past two weeks since the US and Israel first struck Iran on February 27.

- WTI crude has surged close to $100/barrel, rising 47% since 2/27 and +72% year to date.

- Brent crude (more of a global benchmark) is above $100/barrel, rising 42% since 2/27 and is +70% year to date.

There’s a lot of commentary around the fact that the US is energy independent, and that is true. The US is the world’s largest producer of oil and now exports more petroleum products than it imports. However, that doesn’t mean too much in the immediate term because US oil companies can sell oil to global customers, and so the largest bid is what determines prices. And right now, there’s a massive bid because of a shortage, as the world has lost anywhere from 10-20% of the daily flow of oil it needs.

Moreover, a lot of the oil produced in the US, Canada, Venezuela, Middle-East, Russia, Norway etc. is of different quality (light sweet, medium sour, heavy sour) and the refineries in different parts of the world use these 3 different oil qualities.

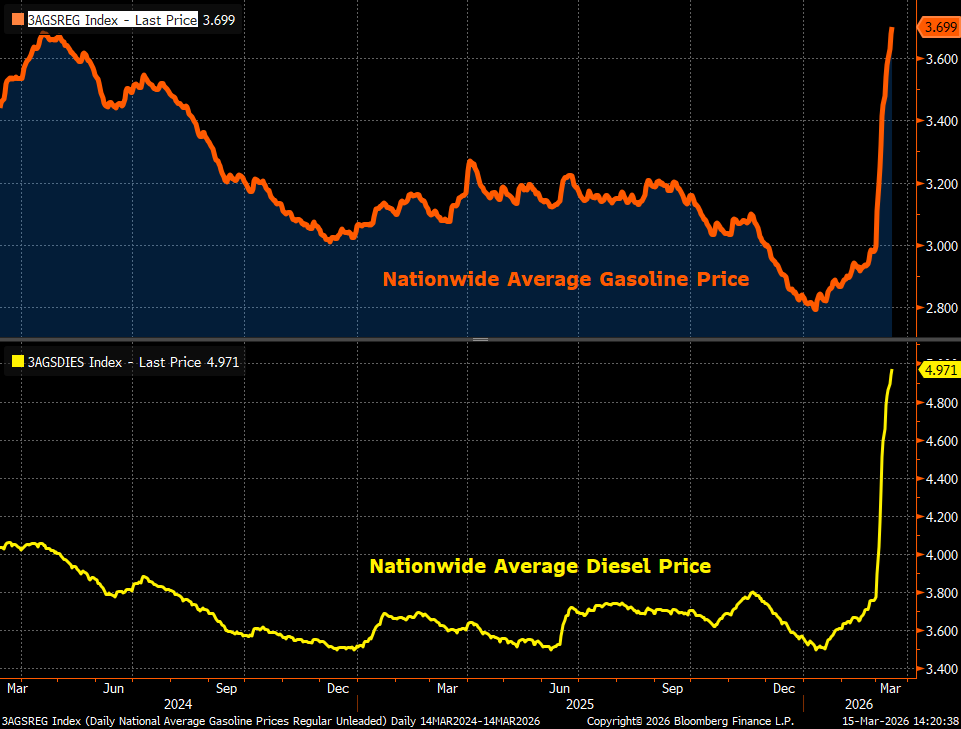

Demand is huge, so gasoline and diesel prices have surged, despite “energy independence.”

- Nationwide average gasoline prices have hit $3.70/gallon, the highest since October 2023. It was $2.80/gall just two months ago. US could very well see $4.0/gallon in a couple of weeks if this continues.

- Nationwide average diesel prices have hit $4.97/gallon, the highest since December 2022. It was under $3.50/gallon two months ago, and it looks like the trajectory is higher.

It would be one thing if the impact were just on gas prices, as a quick resolution to the conflict, could send prices the other way (lower), but it’s not.

- Higher diesel prices will put upward pressure on food prices, as diesel is used to transport food.

- Fertilizers are made of urea, and that’s being disrupted by blocked exports from the Middle East. Fertilizer costs are surging, and that will feed its way into the global food production system later this year.

- Fuel prices are surging across the globe, sending container freight costs higher than what we saw in 2008 and 2022, and that will pass through to goods prices (and inflation).

The decrease in the oil available is already disrupting the production of several products derived from petroleum (in addition to the ones mentioned above). Returning to normal will take several weeks, even if the crisis ended today. And the longer the crisis continues, the greater the ongoing disruption and time required to get back to “normal.”

Rate Hikes Are Back on the Menu

As I pointed out above, the inflation picture wasn’t pretty even prior to the crisis. Just based on that, the odds of any further interest rate cuts by the Fed this year would be much lower or rather dissapeared. The markets are coming around to this outlook as well.

US had anything but price stability now, and the outlook does not look great. Don’t be surprised if the Fed starts talking about the possibility of raising interest rates sooner rather than later.

The key factor, from a market perspective, is how long the conflict lasts, how much damage is done to oil infrastructure in the process, and how long the Strait of Hormuz remains closed. For now, we are all still watching for a resolution in weeks rather than months, but the effects will be stickier, the longer the conflict lasts.