Summary:

- Atomera specializes in developing and licensing proprietary technologies for the semiconductor industry, with a focus on its Mears Silicon Technology.

- The company’s strong business connections and significant cash position make it an attractive investment opportunity.

- Atomera’s technology has the potential to improve chip efficiency and performance in growing markets like 5G and IoT, which could lead to significant net sales growth.

Atomera Incorporated (NASDAQ:ATOM) recently reported significant exposure to the AI industry, 5G, and the IoT sector, which may, in my view, accelerate net sales growth. Taking into account the number of customer engagements expected for the year 2024, the business connections of ATOM’s CEO, and total amount of cash standing in the balance sheet.

Atomera: Technologies For The Semiconductor Industry.

Atomera specializes in developing, commercializing, and licensing proprietary technologies for the semiconductor industry, with a strong focus on its technology, Mears Silicon Technology or MST.

MST consists of a thin film of redesigned silicon, which improves the performance of CMOS transistors, commonly used in industry. MST is expected to enable the manufacturing of smaller, faster, and more energy-efficient transistors.

It is worth noting that the company does not manufacture integrated circuits directly, but offers low-cost solutions to designers and manufacturers. Its customers include foundries, IDMs, fabless manufacturers, OEMs, and electronic design automation companies.

In the last quarterly report, Atomera noted that it is launching products for the massive semiconductor market, which is worth around $550 billion. Besides, management noted that it is creating a patent portfolio that will most likely generate revenue thanks to a licensing business model.

Solid Balance Sheet

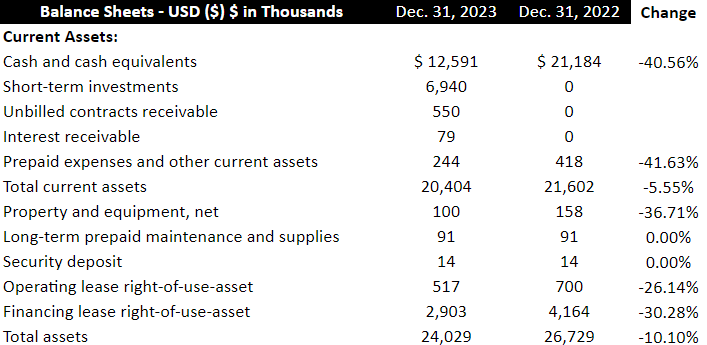

In the last quarter, the company reported a significant amount of cash and short-term investments. More than 70% of the total amount of assets is represented by cash in hand and short-term investments. Atomera is well-prepared to invest in sales, marketing, R&D, and hiring new personnel. The current ratio is larger than one, and the asset/liability ratio appears very healthy. In particular, the company noted cash worth $12 million, short-term investments worth $6 million, total current assets of about $20 million, and total assets of about $24 million.

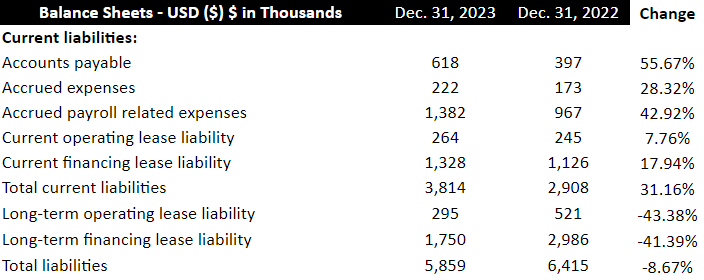

The list of liabilities does not seem at all worrying because Atomera does not report debt. With current financing lease liability worth $1 million, total current liabilities close to $3 million, and long-term financing lease liability of about $1 million, total liabilities stand at $5 million. In sum, we are talking about a company that has negative net debt.

My Opinion

Atomera’s financial position reflects a significant amount of cash, which will most likely help the company focus on the development and licensing of its MST technology. With revenue coming from new deals and collaborations, the company seeks to capitalize on its competitive advantage in the semiconductor industry. I also believe that exposure to the AI industry, 5G, and the IoT sector could serve as net sales catalysts in the next nine years. Although the company faces challenges such as uncertainty in MST adoption, prudent risk management and diversification of partnerships mitigate these aspects. Future financial success will depend on the efficient execution of the strategy and the continuation of profitable partnerships in a dynamic market. With all that being said, I believe that there is more upside potential in the stock price than downside risks.